Date: 28th May 2024.

Market News – Stocks Mixed, USD Down ahead of crucial inflation data later this week.

Economic Indicators & Central Banks:

Financial Markets Performance:

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stocks Mixed, USD Down ahead of crucial inflation data later this week.

Economic Indicators & Central Banks:

- ECB officials continue to flag a June cut, but even ECB chief economist Lane, hardly one of the hawks, stressed that policy settings will likely have to remain restrictive for the rest of the year. ECB’s Schnabel wants to reserve QE for moments of crisis. Villeroy says ECB shouldn’t rule out July cut.

- Lagarde will have to perform a difficult balancing act next week, to convince markets that all options remain open for the second half of the year.

- FT reported: Chinese property developers saw their shares rally in recent weeks after Beijing announced a real estate support package, but have subsequently sold off amid concerns the measures will not be enough to help the stricken sector.

- Japan’s service prices rose 2.8% year-on-year, the fastest increase in over 30 years, indicating a broadening inflation trend. This jump, surpassing economists’ 2.3% forecast, supports the case for the Bank of Japan to raise interest rates. The BOJ sees service prices as crucial for gauging inflation spread. This data may prompt the BOJ to consider an earlier rate hike, with some forecasts suggesting a possible move by July.

- Chinese equities declined with real estate companies dragging down the country’s benchmark index.

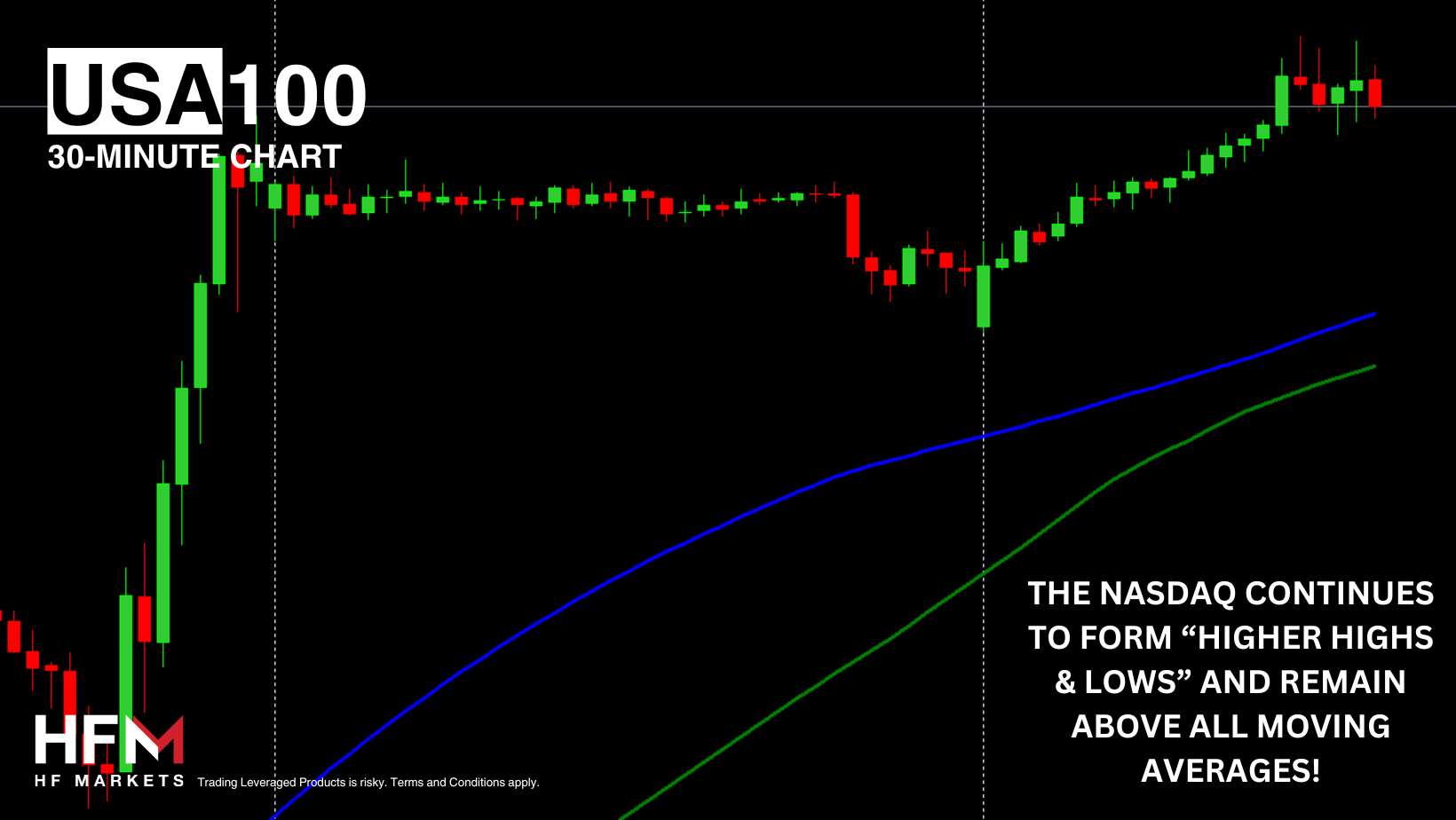

- European & US futures arehigher as the Dollar slipped before a swath of inflation prints that’s expected to influence the direction of global monetary policy.

- All eyes this week are on fresh inflation data from Australia to Japan, the euro region and the US. The ECB is set to release its April CPI expectations later in the day.

Financial Markets Performance:

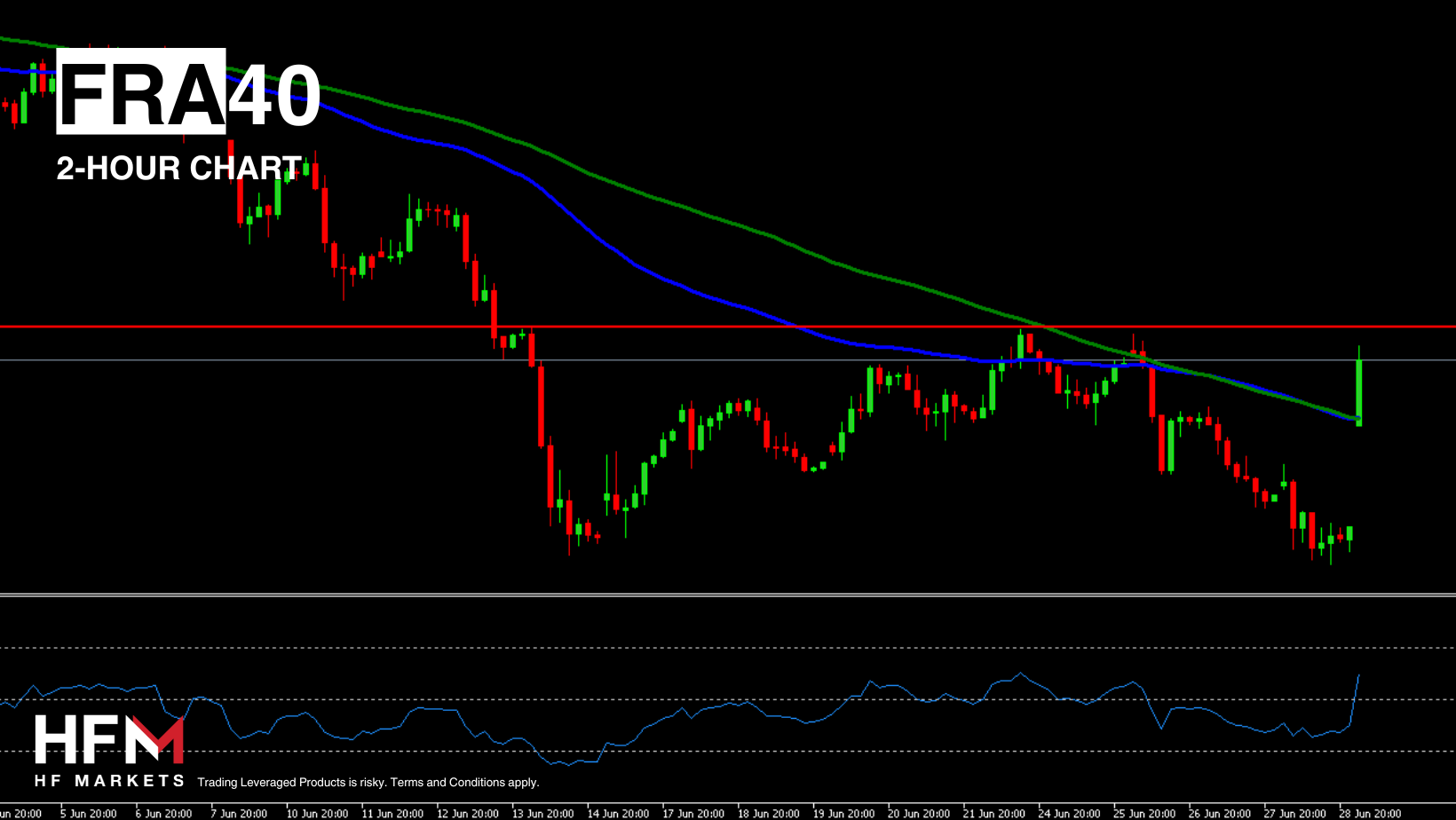

- The USDIndex slipped for a 2nd day, retesting 6-month trendline. Currently set at 104.35.

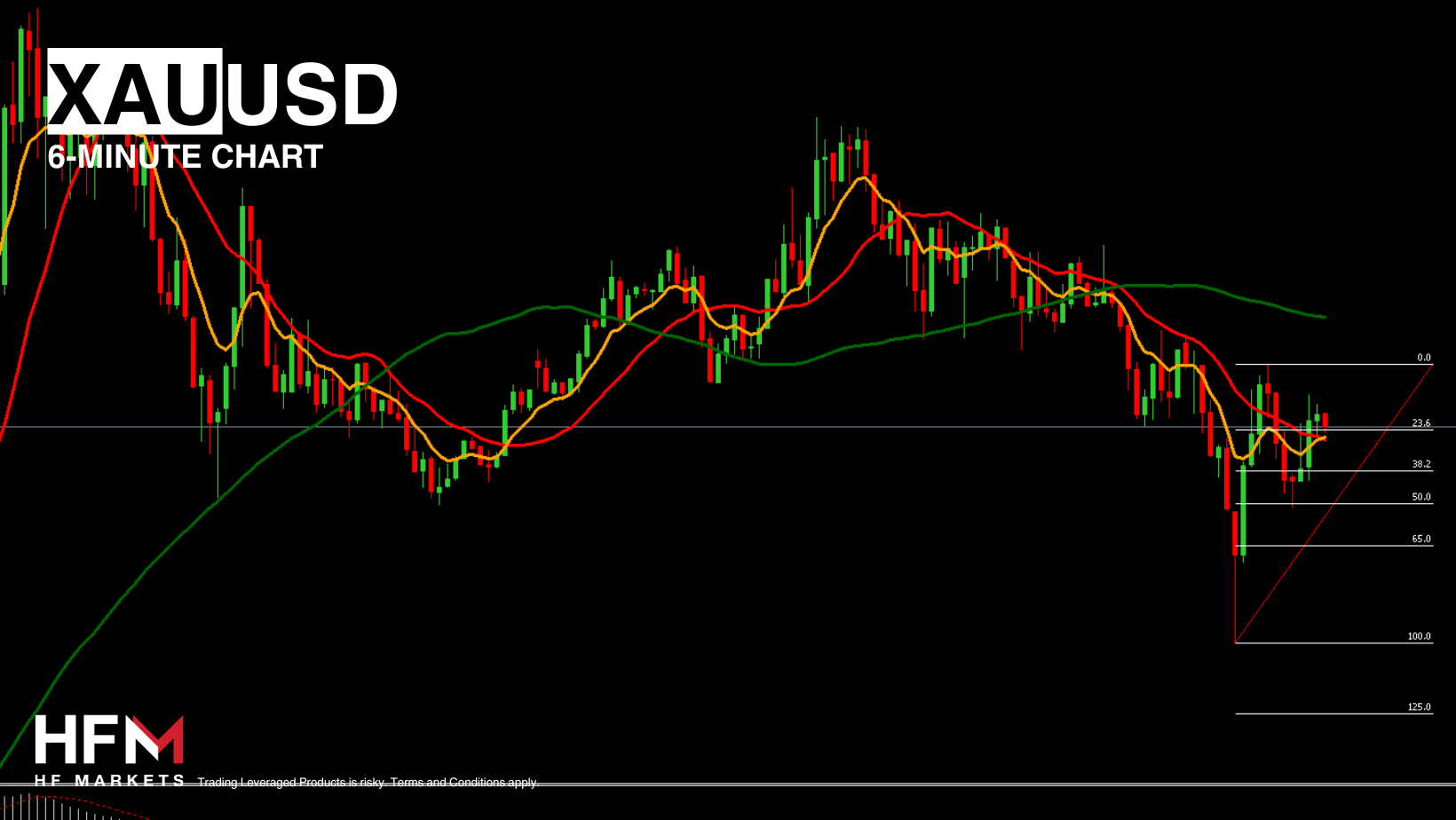

- Gold prices remained steady as the Dollar eased, with investors eyeing key US inflation data for hints on potential Fed rate cuts. Spot gold held at $2,342 per ounce.

- Oil prices steadied after 2 days of gains, i.e. at $78.70, despite rising Middle East tensions following the death of an Egyptian soldier in a clash with Israeli troops. Overall, prices have dipped since early April due to weakening demand from Asia, leading Brent’s prompt spread close to a contango structure, signaling increasing supply relative to consumption.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.