Date : 29th November 2022.

Market Update – November 29 – Tightening Tilt, COVID Control & Month End Flows.

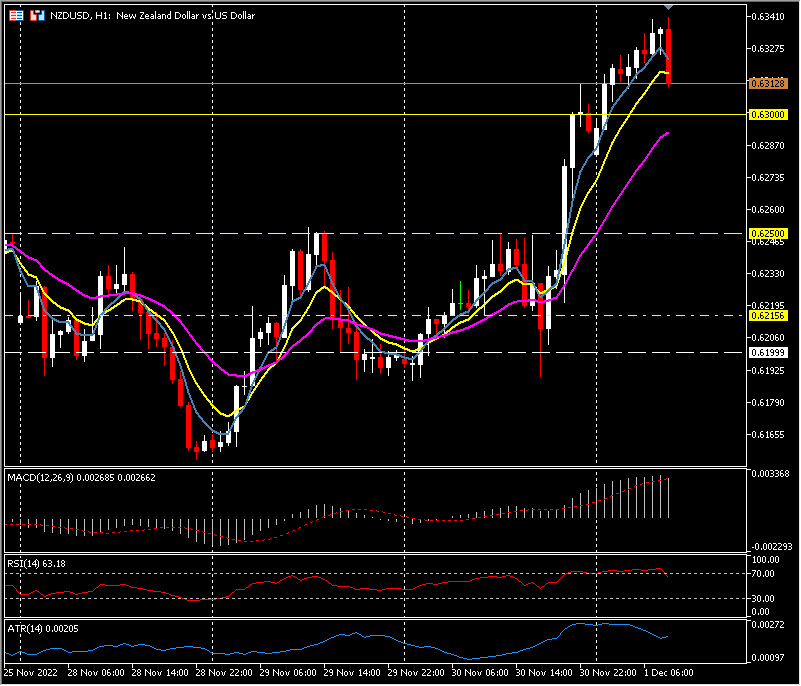

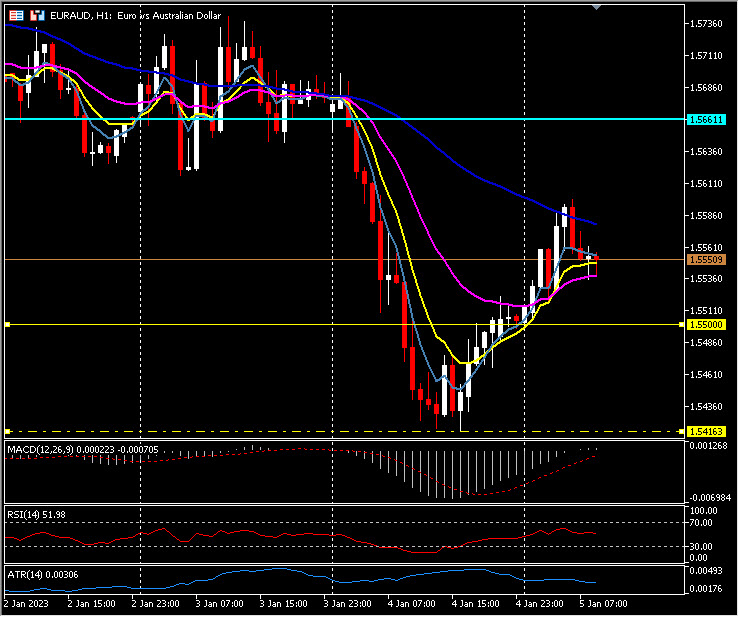

Biggest FX Mover @ (07:30 GMT) NZDUSD (+1.10%), bounces to 0.6235. MAs aligning higher and RSI at 63 but MACD histogram & signal line remain below 0. H1 ATR 0.00147, Daily ATR 0.00962.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

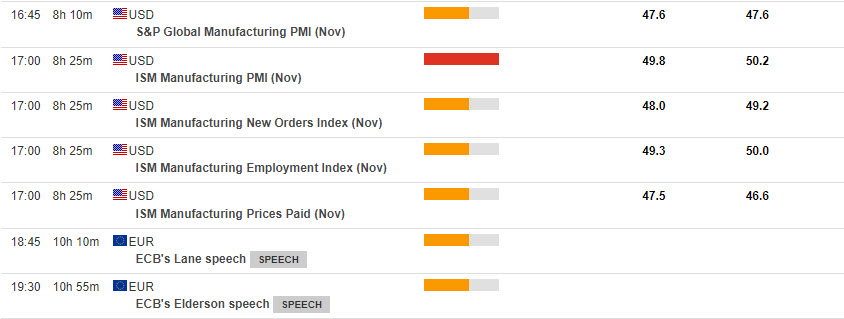

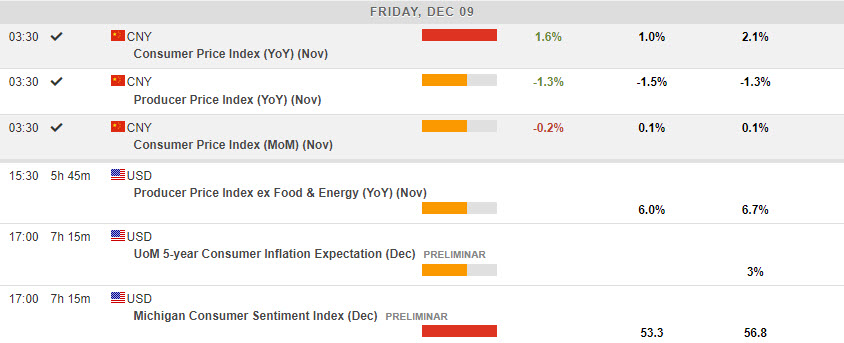

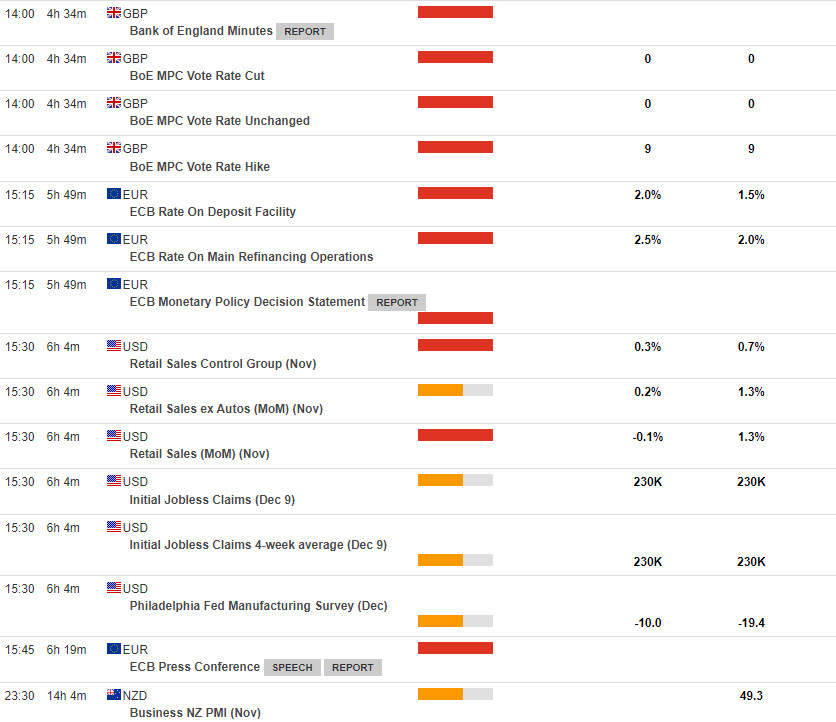

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – November 29 – Tightening Tilt, COVID Control & Month End Flows.

- The USDIndex rallied to 106.70 in the previous session but formed a correction in Asia session to 106.00 ahead of a COVID-19 press briefing in China that is spurring hopes of a potential easing in the country’s strict pandemic restrictions.

- Fed Officials Signal Higher rates: Hawkish reminders from key Fed officials Williams, Bullard, and Brainard that rates will have to go higher helped weigh on the markets in Monday action. Wall Street was weaker overnight on the back of Williams’s and Bullard’s comments, and slipped further as Brainard tripled down on the rate outlook.

- US houses prices fall like in 2008.

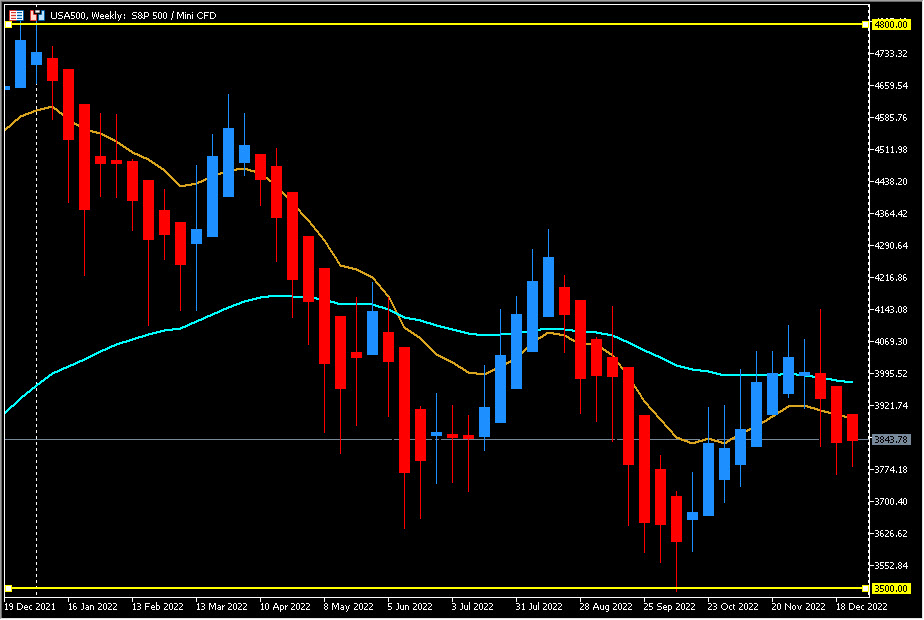

- Stocks – Global stocks rise after yesterday’s dip. US100 and US500 dropped -1.58% and 1.54%, respectively, with the US30 off -1.45% amid broadbased weakness. Today however the rumours of an earlier easing of strict COVID-19 restrictions along wihth vaccinations for over 80-year olds, found buyers in the stock market with a Chinese stocks rebound. Hang Seng and CSI 300 bounced 4% and 3% respectively. ASX and Nikkei closed narrowly mixed. GER40 and UK100 futures are up 0.5% and 0.4% respectively.

- EUR – reversed from 5-month peak. Currently at 1.0360. ECB’s Lagarde said overnight that inflation had not peaked and it risks turning out even higher than currently expected, hinting at a series of interest rate hikes ahead.

- JPY along with Yuan, Aussie and Kiwi on bid.

- GBP – turns again below 1.20 at 1.1987.

- USOil – jumps to 80.00 as China refines its approach for dealing with protest and Covid control. All eyes are on weekend OPEC+ meeting. EU fails to agree on Russian oil price cap once again.

- Gold – fully recovered yesterday’s losses, currently at $1754.

Biggest FX Mover @ (07:30 GMT) NZDUSD (+1.10%), bounces to 0.6235. MAs aligning higher and RSI at 63 but MACD histogram & signal line remain below 0. H1 ATR 0.00147, Daily ATR 0.00962.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.